Tag: geopolitics

-

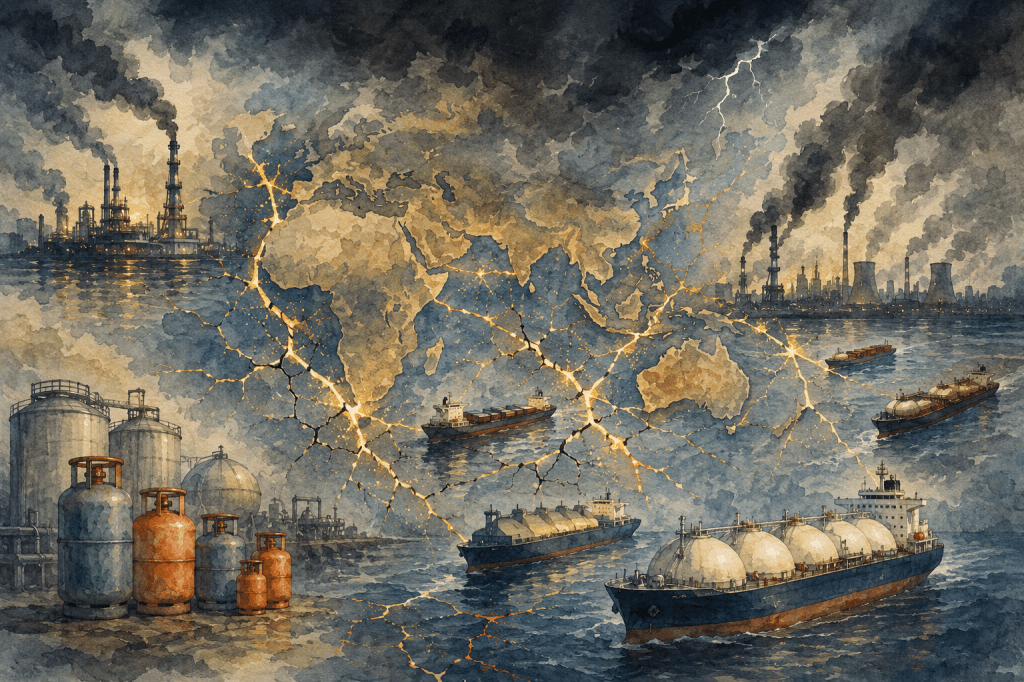

A Cauldron of Gases – Part 3: The Geopolitics of the Flame – Supply Chains, Vulnerabilities and Power

The article explores the intricate geopolitics of energy supply chains, emphasizing vulnerabilities and dependencies shaped by geography, insurance markets, and political stability. Key disruptions, especially in the Strait of Hormuz and other chokepoints, significantly affect global energy prices and ultimately impact ordinary households, revealing the fragility of modern energy systems.

-

A Cauldron of Gases – Part 2: The Geopolitics of the Flame – The Chokepoints

In an ideal world, liquids and gases, unless restrained, flow freely. However, we do not live in a Utopia. So, in the real world, geography charts (and constrains) the flow of water on the Blue Planet. Some of the important pieces in this unique geographical jigsaw are…

-

A Cauldron of gases

Part 1 Dramatist Personae – the Gases Recent events in the Persian Gulf have brought to the fore discussions on energy and by extension, fuel and gases. Though they do not figure in the calculation of core inflation, their production and supply have worldwide ramifications. It is necessary to understand what these gases are, how…