The Geopolitics of the Flame: Supply Chains, Vulnerabilities and Power

If Part 2 examined the geography through which energy flows, Part 3 examines what happens when those flows are disrupted, delayed or weaponised.

Globalisation created the impression that energy flows freely across the world. The reality is more complex. Oil, LNG and LPG move through narrow maritime arteries, constrained by geography, protected by navies, insured by global financial markets and dependent upon political stability. The modern energy economy resembles less a reservoir and more a circulatory system. When arteries narrow, pressure rises everywhere — and it reaches ordinary households, long before the television anchors begin to explain why.

The world is not as flat as we would like it to be !

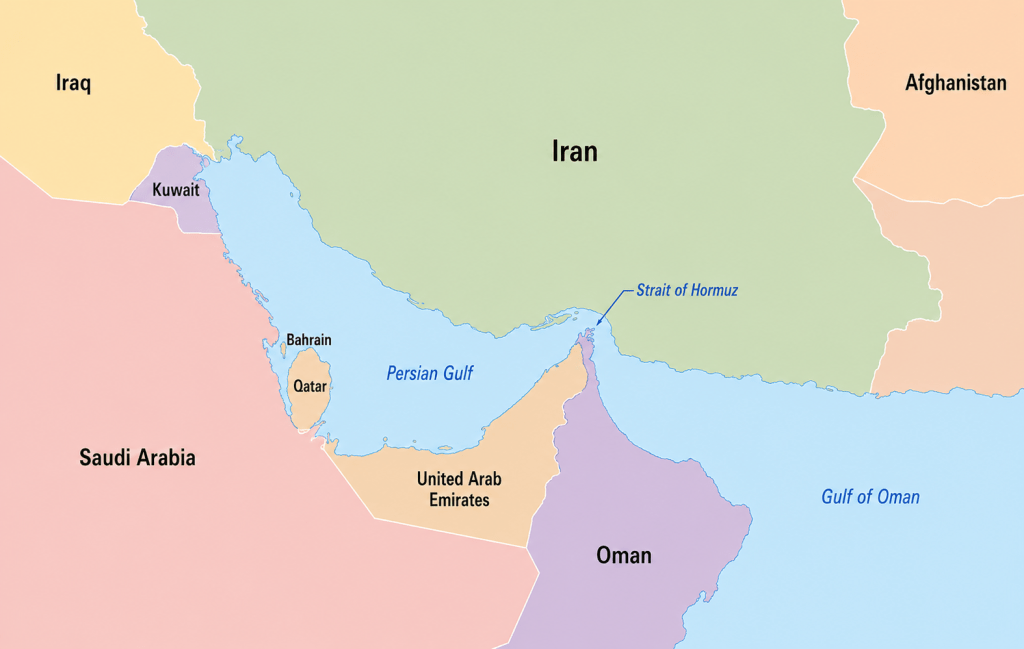

a) Hormuz: When the Valve Tightens — and the Insurer Leaves the Room

While much public attention during crises focuses on oil and gas production, the immediate disruptions are often logistical — and, increasingly, financial. The events of early 2026 around the Strait of Hormuz offered a remarkably instructive lesson in how modern energy vulnerability actually works.

Within forty eight hours of the intensification of conflict in the Gulf in February 2026, war risk insurance premiums surged fivefold. Major marine insurers terminated existing coverage. Lloyd’s Joint War Committee — a body that quietly governs the risk architecture of global shipping — redesignated the entire Arabian Gulf as a conflict zone. Tanker traffic collapsed by more than 80 percent. Not because the Strait was physically blocked. Because it had become commercially uninsurable.

This is the insurance weapon — and it operates faster than any navy. In normal times, war risk insurance for a large crude tanker worth $100 million costs roughly $150,000 to $225,000 per voyage. By March 2026, premiums had surged to between 1% and 7.5% of vessel value — translating to between $1 million and $9 million per single voyage. For a ship operator running thin margins, this is not a cost adjustment. It is a commercial death sentence.

The physical consequences follow swiftly. If Hormuz is threatened or partially disrupted, tankers face delays of 7–15 days or more. Freight rates spike. Spot cargo markets tighten. The effects extend far beyond hydrocarbons. India’s imports of petrochemicals, plastics feedstock, fertilisers and industrial chemicals face shortages or cost escalation. Gulf ports slow the movement not only of fuel but of consumer goods, machinery, electronics and food. Hormuz is therefore not merely an oil corridor. It is a strategic valve for inflation stability, industrial supply chains and household welfare simultaneously.

If the Persian Gulf is the reservoir, Hormuz is the tap. And the insurance market is the hand that now sits upon it.

b) Futures, Benchmarks and the Price Before the Price

Before oil or gas arrives at an Indian import terminal, its price has already been determined — not at the wellhead, not even at the port, but in the global futures markets.

Three benchmarks govern the world’s LNG price universe. Henry Hub, traded in the United States, sets the price of American natural gas. The Title Transfer Facility, known as TTF, does the same for Europe. The Japan-Korea Marker, or JKM, is the Asian equivalent — the number that India watches most closely.

These are not merely price indicators. They are the pulse points of the global energy body. Just as a cardiologist reads the pressure differentials to understand where blood is flowing and where it is not, energy traders read the spread between these three benchmarks to decide where gas will move next. When the Asian pulse beats stronger than the American one — when JKM prices run well above Henry Hub — gas flows eastward. When that differential narrows, the flow redirects. Cargoes that might have reached India quietly pivot toward Europe instead, and Asia finds itself competing harder for supply.

India sits at the receiving end of this calculus. The country’s state-owned importers have historically preferred long-term contracts over active financial hedging, which offers stability in normal times but leaves India more exposed when global price signals shift rapidly.

Markets complicate an already complicated geography !

c) The Gulf Dependency Paradox: Why Diversification Exists on Paper

India has gradually diversified its energy suppliers. LNG and LPG cargoes increasingly arrive from the United States, Australia and other producers beyond West Asia. GAIL holds long-term contracts for 5.8 million tonnes of LNG annually from US terminals. India’s LNG imports from the US stood at $2.46 billion in 2024-25, a 74 percent increase from the year prior, making it the second-largest LNG supplier. Yet geography continues to exert its own stubborn logic.

A voyage from the US Gulf Coast to India can take up to 45 days, compared with less than a week from the Gulf. This is not merely a matter of time — it is a financial multiplier. LNG carriers are among the most expensive commercial vessels in the world. A modern cryogenic tanker capable of maintaining temperatures below minus 160 degrees Celsius can cost well over $200 million to construct and typically commands charter rates of tens of thousands of dollars per day. Every additional day at sea increases financing, insurance and opportunity costs.

A voyage lasting forty days therefore ties up a vessel several times longer than an equivalent Gulf route. Freight costs for US-origin LNG and LPG delivered to India are consequently often two or more times higher than comparable Gulf cargoes.

The LPG market illustrates this particularly well. During periods of disruption, freight rates on routes from the US Gulf Coast to Asia can rise dramatically as buyers seek alternative supplies and vessels become scarce. Longer routes, congestion at strategic waterways and occasional rerouting around the Cape of Good Hope further increase costs. Geography, once again, reasserts itself. A molecule of gas may be identical whether it originates in Texas or Qatar, but the economics of moving it are profoundly different.

The valve seems irreplaceable for now !

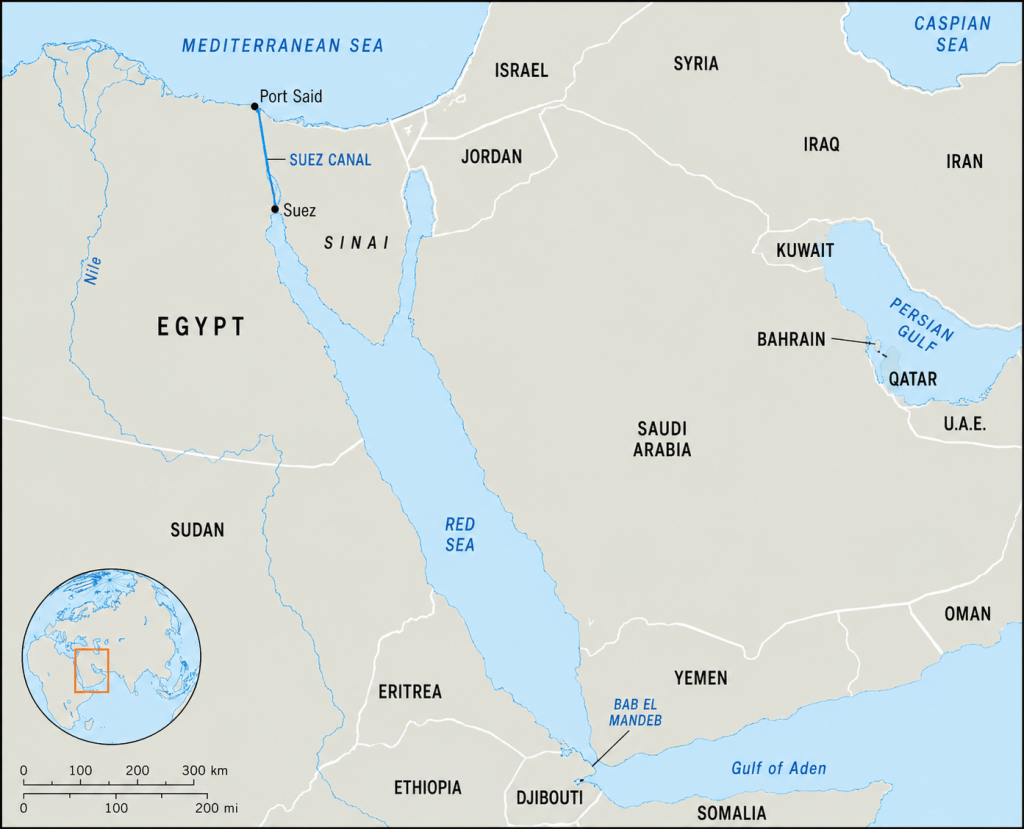

d) Suez and the Red Sea: The Cost of Distance

Unlike Hormuz, where vulnerability is immediate and concentrated, disruptions in the Suez-Red Sea corridor operate more subtly — through time, distance and cost.

The strategic value of the Suez Canal lies in its role as the shortest maritime route between the Atlantic and Indian Ocean systems. Any disruption in the Red Sea-Suez corridor may force vessels to reroute around the Cape of Good Hope, adding roughly 3,500–5,000 nautical miles and approximately 10–14 days of transit time. The detour substantially increases fuel consumption, vessel utilisation costs, freight rates and insurance premiums. During recent Red Sea disruptions, shipping analysts estimated that a single Gulf-to-Europe voyage could incur several hundred thousand dollars to over a million dollars in additional fuel costs alone, even before war-risk surcharges were taken into account.

Recent instability around Bab-el-Mandeb demonstrated that even if the Suez Canal itself remains operational, insecurity in adjoining waters can reduce vessel traffic significantly. For India, the Suez route remains critical for trade with Europe, westbound exports, and alternative supply lines for US and Atlantic Basin LNG cargoes. Suez disruptions rarely stop trade entirely — they make trade slower, costlier, and less predictable.

One may even salute Monsieur Lesseps for his foresight to build the Suez !

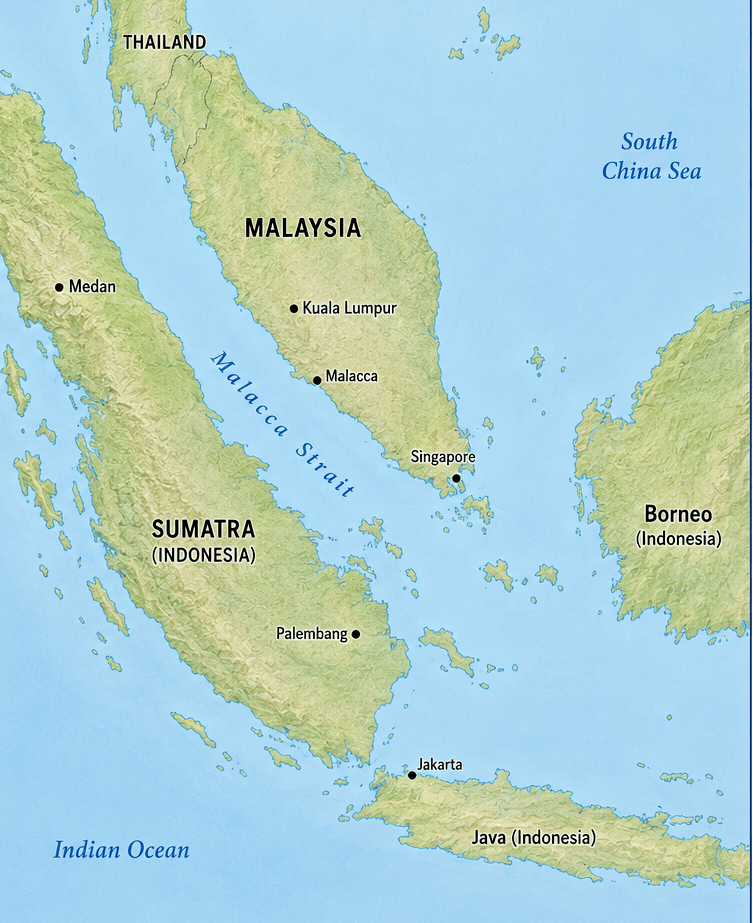

e) Panama and Malacca: Climatic and Great-Power Vulnerabilities

The Panama Canal and the Strait of Malacca reveal that not all chokepoints are vulnerable in the same way — and not all threats wear war colours.

The Panama Canal depends heavily on freshwater from surrounding lakes to operate its complex lock system. Drought conditions linked to El Niño have periodically forced restrictions on vessel transits and cargo loads — a reminder that in an era of climate change, geography itself can become less reliable. Since the American shale boom, the canal has become strategically important for LNG and LPG cargoes moving from the US Gulf Coast to Asia. A typical voyage from the US Gulf to Japan takes roughly 20–25 days via Panama, compared with more than 30 days via the Cape of Good Hope. During the recent drought-induced congestion, priority transit slot auctions reportedly reached approximately $1.76 million per vessel, illustrating how quickly a chokepoint can evolve from a passageway into a price-setter.

Malacca presents a different challenge altogether. Stretching between Malaysia and Indonesia, it carries roughly one-quarter of global maritime trade and is central to the energy security of China, Japan and South Korea. The ‘Malacca Dilemma’ — China’s strategic anxiety about this bottleneck — has partly driven Beijing’s investment in alternative overland pipelines, ports and Belt and Road corridors. For India, Malacca represents the eastern gateway connecting the Indian Ocean to the Pacific trading system, which is why the Andaman and Nicobar Islands occupy such a pivotal position in India’s maritime calculus.

f) How the Shock Reaches Ordinary People

The consequences of geopolitical disruption eventually travel from distant seas into ordinary households — and the transmission mechanism is faster and more direct than most of us appreciate.

A disruption at Hormuz increases war-risk insurance premiums, which are passed through to shipping costs, which are passed through to the landed cost of crude oil, LNG and LPG. Oil marketing companies face higher import bills. The LPG subsidy burden on the government rises. Cylinder prices come under pressure. Simultaneously, LNG price increases affect fertiliser production because natural gas is the primary feedstock for urea manufacturing. Rising fertiliser costs eventually reach food prices on every table.

The result is not merely an energy issue, but an inflationary one. Energy geopolitics manifests itself in something as ordinary as the monthly household budget — a connection that is almost never articulated in the breathless television coverage of maritime conflicts.

So non-core inflation becomes a core headache!

g) India’s Strategic Vulnerability Hierarchy

Not all fuels occupy the same strategic position in India’s energy architecture, and it is worth mapping the hierarchy clearly.

Crude oil is macro-critical. Its disruption affects transport, inflation, foreign exchange reserves and the broader economy. India’s strategic petroleum reserves provide a limited buffer — but no equivalent strategic reserve exists for LNG or LPG.

LPG is politically sensitive. With over 320 million household connections, its affordability is directly tied to welfare and social stability. A sustained price shock in LPG cylinders is felt more immediately and viscerally by India’s population than a comparable shock in any other energy category.

LNG forms the industrial backbone. Fertiliser production, power generation and manufacturing depend upon it. A prolonged disruption does not merely raise prices — it can slow food production and industrial output in ways that compound over months.

Together, these three fuels constitute the energy vulnerability architecture — and exposure to a single corridor, the Strait of Hormuz, cuts across all three simultaneously.

h) Efficiency versus Resilience: The Trade-off Globalisation Made

Modern energy systems frequently trade resilience for efficiency. The same globalisation that lowered costs also reduced buffers. As supply chains became leaner and faster, they simultaneously became more fragile. This is the central tension of our energy future: we may not be able to afford the cost of American LNG at scale, cannot build stockpiles overnight, and cannot decouple from the Gulf without paying a price — financial, logistical and strategic — that would dwarf any short-term political calculus.

The modern world often imagines energy as something produced in distant deserts or offshore rigs. In reality, energy is sustained by a fragile choreography of geography, shipping lanes, ports, insurers, futures markets and political stability. From Hormuz to Malacca, from Suez to Panama, narrow waterways silently shape inflation, industrial output and household welfare across continents. And the insurance market, it turns out, can close a strait faster than any navy ever could.

In the twenty-first century, the geopolitics of energy is no longer merely about who owns the resources — but about who controls, protects and sustains the arteries through which they flow, and who pays when they falter.